Updated with Recent Court Rulings (2025-26)

Capital gains tax planning is essential for real estate investors, property developers, and high-net-worth individuals in India. When selling residential or commercial property, the eligibility for tax exemptions under Sections 54 and 54F of the Income-tax Act, 1961 depends critically on the type of property sold and the type of property acquired.

This article provides an authoritative analysis of capital gains tax rules with recent judicial clarifications, practical investor insights, and case studies. It is aimed at real estate investor blogs and chartered accountant (CA) advisory platforms.

Capital Gains Tax Framework (India)

Classification

- Short-Term Capital Gain (STCG): Held less than 24 months

- Long-Term Capital Gain (LTCG): Held 24 months or more

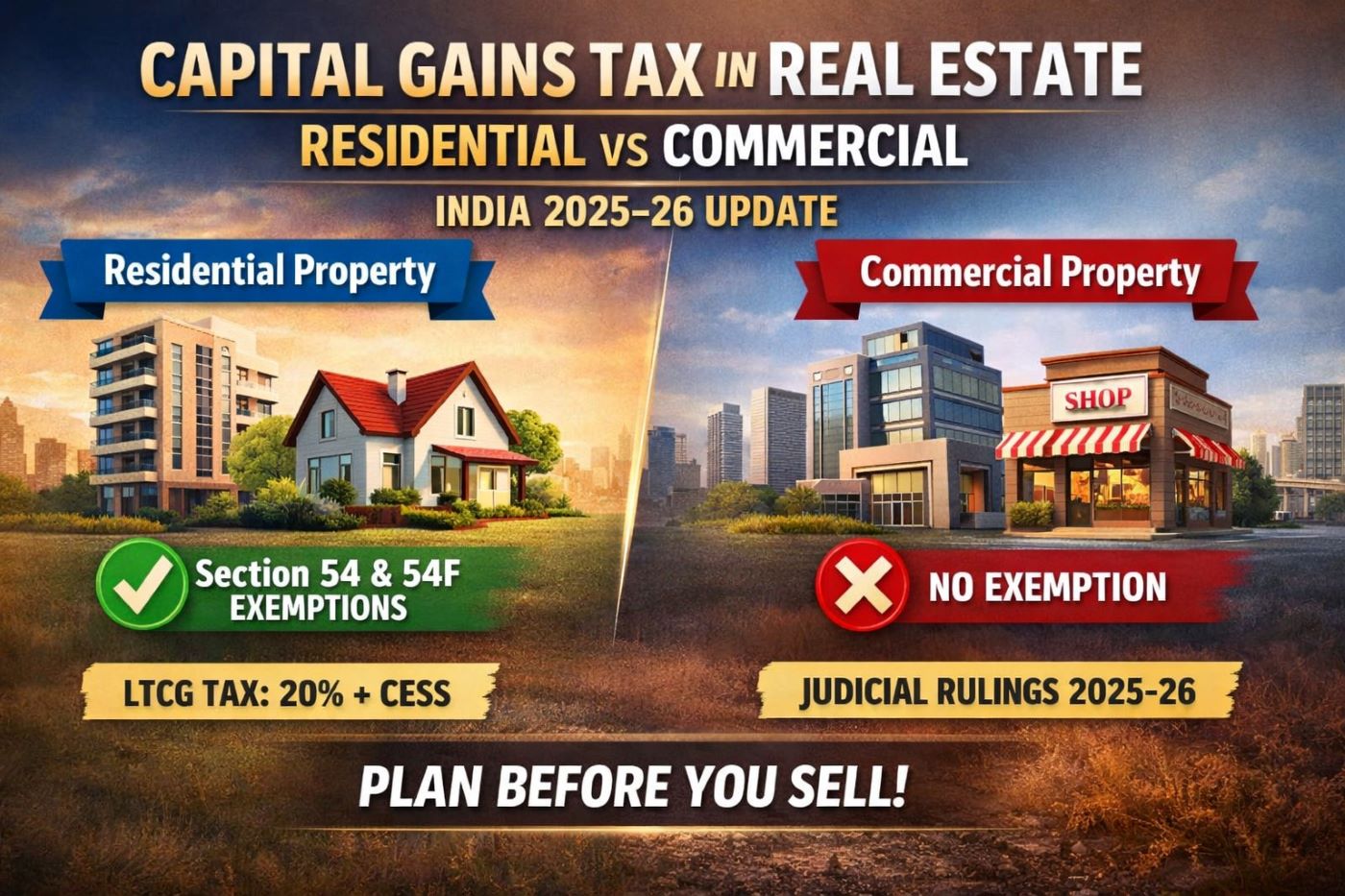

- LTCG Tax Rate: 20% + cess with indexation benefit

Only LTCG qualifies for exemptions under Sections 54 and 54F.

When You Sell Residential and Buy Commercial Property

Tax Implication:

No exemption under Section 54 or 54F if reinvested into a commercial asset.

Reason:

- Section 54 applies only if both the sold and acquired assets are residential houses or apartments.

- Commercial properties such as offices, retail shops, or warehouses do not qualify as replacement assets for Section 54 exemptions.

Investor Case:

Selling a residential flat and using the capital gains to acquire an office unit means the entire LTCG becomes taxable at 20% + cess.

When You Sell Commercial and Buy Residential Property

Tax Implication:

Exemption available under Section 54F, if conditions are complied with.

Key Conditions

- Original asset sold is not a residential house.

- Entire net sale consideration must be reinvested in one new residential house within:

- 1 year before sale, or

- 2 years after sale, or

- Construction completed within 3 years.

Recent Judicial Clarifications

- Delhi High Court (2025) – Clarified that multiple floors purchased in the same building may be treated as one residential house for Section 54F purposes when used as a single residential unit.

- ITAT Ahmedabad (Dec 2025) – Ruled that a penalty imposed for incorrect calculation of Section 54F exemption does not constitute misreporting of income, offering relief to taxpayers who make genuine calculation errors.

- ITAT Mumbai (Jan 2026) – Upheld exemption under Section 54F even when the sale agreement was delayed by the builder, confirming that genuine reinvestment timing (through bank payments/cheques) is critical, not formal agreement execution dates.

When You Sell Commercial and Buy Commercial Property

Tax Implication:

No exemption under Sections 54 or 54F.

Explanation:

- Section 54 applies only to residential-to-residential transactions.

- Section 54F applies when non-residential capital gains are reinvested into residential property only.

Investor Case:

Selling a retail shop and reinvesting in another shop results in full taxable LTCG.

When You Sell Residential and Buy Residential Property

Tax Implication:

Exemption available under Section 54, subject to conditions.

Conditions for Section 54 Exemption

- New residential property bought within 1 year before or 2 years after sale, or constructed within 3 years.

- Limit of exemption capped at ?10 crore from AY 2024-25 onward.

Judicial Developments

- ITAT Mumbai (Apr 2025) – Allowed exemption of ?1.3 crore under Section 54 to a husband-wife duo who jointly acquired a new residential property using proceeds from sale of two houses, reinforcing that joint ownership does not disqualify exemption eligibility if the transaction and investment are genuine.

- ITAT (2024) – Held that Section 54 relief is valid based on the possession date of the new property, not just the agreement date, influencing compliance strategy for capital gains exemption timing.

Capital Gains Account Scheme (CGAS)

If the new residential or commercial property is not acquired before filing the income tax return, the unutilized capital gain must be deposited in a Capital Gains Account Scheme (CGAS) to preserve exemption eligibility. Failure to do so results in disallowance of the exemption claimed.

| Sold Asset | Acquired Asset | Exemption | Applicable Section |

| Residential | Residential | Yes (with limits) | Section 54 |

| Residential | Commercial | No | — |

| Commercial | Residential | Yes (conditions) | Section 54F |

| Commercial | Commercial | No | — |